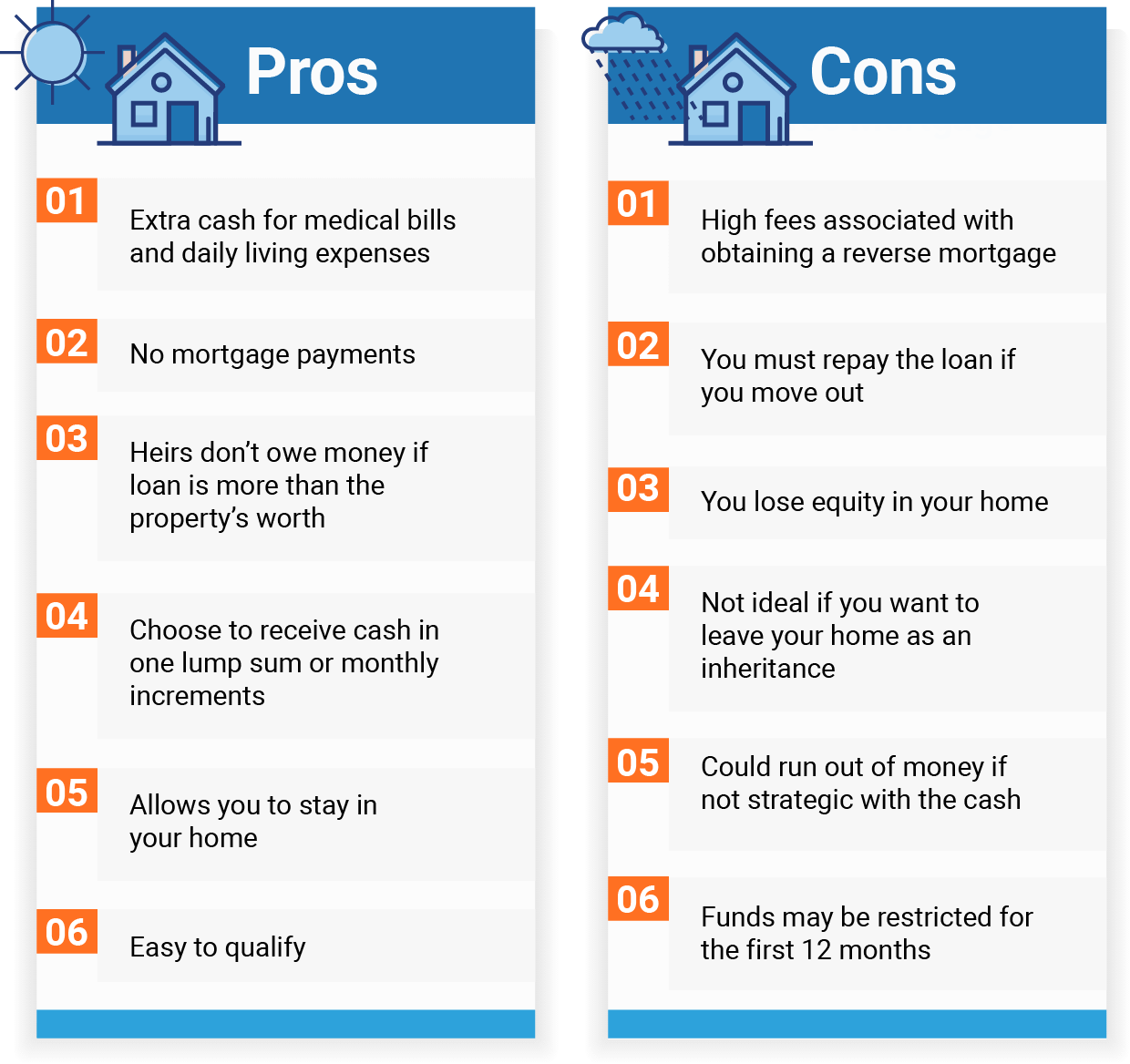

After the reverse home mortgage proceeds settle the existing home mortgage, the foreclosure stops and you will not need to make any more month-to-month payments. Sounds quite good, ideal? However there are disadvantages to using a reverse mortgage in this way. One drawback is that the debtor loses some or many of the equity that's developed throughout the years.

Also, the reverse home mortgage loan provider can call the loan due if and when one of the following occasions takes place: The borrower permanently vacates the house. The borrower moves out of the house short-term due to a physical or mental disorder, and is gone for over a year. The customer offers the home or deeds the home to a brand-new owner.

(If a certified https://www.canceltimeshares.com/blog/how-do-i-cancel-a-timeshare/ non-borrowing partner still resides in the house, the lending institution can't call the loan due under specific circumstances). The borrower doesn't satisfy the home loan requirements, like paying real estate tax, having house owners' insurance coverage on the property, and keeping the home in good condition. what do i need to know about mortgages and rates. Once the lending institution calls the loan due, the loan needs to be paid back or the lending institution will foreclose.

A reverse home loan is only one method to avoid a foreclosure. A couple of other choices to consider are: re-financing the existing home mortgage getting a home mortgage adjustment, or offering the home and moving to more budget friendly lodgings. The Customer Financial Defense Bureau uses a helpful reverse mortgage discussion guide and encourages consumers who are considering taking out a reverse mortgage to consider all other options - which mortgages have the hifhest right to payment'.

Top Guidelines Of How Is The Compounding Period On Most Mortgages Calculated

Even though you'll need to finish a therapy session with a HUD-approved therapist if you wish to get a HECM, it's likewise highly recommended that you consider speaking to a financial organizer, an estate preparation lawyer, or a consumer defense lawyer prior to getting this type of loan - find out how many mortgages are on a property.

A new in-depth investigation on foreclosure actions related to reverse home loans released late Tuesday by U.S.A. Today paints a bleak photo surrounding the activities and practices of the reverse home mortgage industry, however also relates some doubtful and obsolete info in crucial locations highlighted by the investigation, according to market participants who talked to RMD.

Describing a wave of reverse home mortgage foreclosures that predominantly impacted metropolitan African-American communities as a timeshare weeks calendar "stealth aftershock of the Great Recession," the investigative short article concentrates on nearly 100,000 foreclosed reverse home mortgages as having "stopped working," and affecting the monetary futures of the customers, adversely affecting the property worths in the communities that surround the foreclosed homes.